Making an impact

Our mission is to improve the competitiveness and prerequisites for operation for businesses in the chemical industry. We do this by actively stating our views on regulation and public funding.

One of the key activities of the Chemical Industry Federation of Finland is advocating important current topics regarding the chemical industry both at the Finnish and the EU level. Our goal is to improve the competitiveness and the operating environment of the industry’s businesses in Finland. Here you can find the key advocacy themes and our advisors’ contacts for more information.

Our members can access further information about the progress of our advocacy efforts in KemiaExtra.

Lobbying and societal impact

Subject Overview

In accordance with the government program of Prime Minister Sanna Marin’s administration, Finland will establish a transparency register (also known as a lobbyist register). The purpose of the law is to enhance transparency in decision-making, thereby combating undue influence and strengthening citizens’ trust.

Chemical Industry’s Objective

The objective of the transparency register is commendable. The register should be under the responsibility of an authority, and it should genuinely improve transparency without unreasonably increasing the administrative burden on those required to report. The regulations should emphasize incentivization rather than disciplinary elements. In the initial phase of implementation, the scope should be limited to Members of Parliament and Ministers, as well as their assistants. If individual meetings are to be recorded (in a meeting diary, so to speak), the responsibility for recording should lie with the decision-maker, i.e., the one being lobbied, not the lobbyist.

Additional Information

Energy and Climate

Subject Overview

In 2018, Ursula Von Der Leyen outlined the introduction of a Carbon Border Adjustment Mechanism as part of the Green Deal, which would apply a tariff or tax on products based on their greenhouse gas emissions. Reporting requirements for products valued at over 150 euros under this mechanism were set to begin on October 1, 2023. Starting from 2026, there will also be an obligation to acquire CBAM certificates to offset the emissions from the production of a product. The obligation to acquire CBAM certificates will increase gradually between 2026 and 2035. The price of CBAM certificates will follow the price of EU emissions trading allowances.

As of the 2023 CBAM decision, products from the chemical industry, including fertilizers (including ammonia) and hydrogen, fall under the scope of the carbon border adjustment mechanism. The current interpretation suggests that the mechanism overlaps with the carbon leakage protection of the EU emissions trading system. Consequently, the allocation of free emission allowances will decrease as the obligation to acquire CBAM certificates increases.

The practical implementation of the carbon border adjustment mechanism appears to pose technical challenges. This topic has also raised concerns from countries outside the EU, with the risk of the situation escalating into a trade dispute.

If the implementation of the carbon border adjustment mechanism is successful, it has the potential to protect the EU’s internal market. However, the loss of free emission allowances (and possible compensation) will negate this benefit for some companies. The carbon border adjustment mechanism does not protect exports, so it seems to be detrimental to industries covered by emissions trading carbon leakage protection.

Objective of the Chemical Industry

The chemical industry approaches the carbon border adjustment mechanism and its potential expansion with caution. The industry believes that the existing carbon leakage protection of the EU emissions trading system should be maintained primarily and strengthened. The EU’s carbon border adjustment mechanism should be kept as narrow as possible, and any potential expansion should be carried out in consultation with the industry affected by the expansion.

The carbon border adjustment mechanism should not affect the cost competitiveness of export industries. Since the mechanism does not protect exports outside the EU, other carbon leakage protections should continue for relevant production. Additionally, the carbon border adjustment mechanism should not be applied to intermediate products in the value chains of chemical industry products. In principle, industries brought within the scope of the mechanism should be granted a sufficiently long transition period now and in the future.

For the chemical industry, it is essential that national authorities interpret CBAM rules and potential sanctions from the EU level reasonably in the early years of the mechanism’s implementation. Additionally, reporting requirements should be designed to minimize additional bureaucracy.

Current Situation and Timeline

The Commission’s CBAM Regulation came into force in 2023, followed by the focus shifting to EU-level and national implementation. The details of the regulation will be further clarified through implementing acts, and several review points have been included in CBAM’s operation, allowing for adjustments to the regulation.

The reporting period for the CBAM Regulation starts from October 1, 2023, to December 31, 2025. After 2026, the obligation to return CBAM certificates begins, with the full obligation being phased in between 2026 and 2035.

What We Influence

-

Finland’s stance

-

European Parliament and Commission

-

Cefic’s stance

-

The activities and positions of the hydrogen cluster

We monitor the positions of other countries and stakeholders and influence the implementation of the mechanism.

Additional information and materials:

Tuomas Tikka

Chief Advisor, Energy and Climate +358 45 131 6683 tuomas.tikka(a)kemianteollisuus.fi Show infoSubject Overview

The Effort Sharing Regulation includes all sectors that generate greenhouse gas emissions outside of the emissions trading sector. In practice, within the EU, the effort sharing sector’s target is divided into member state-specific objectives, and member states must develop measures to achieve these objectives. The Commission monitors the progress of member states and provides recommendations for additional measures through the governance regulation if necessary.

In the spring of 2023, the effort sharing sector’s 2030 target was raised to 40%. Finland’s national target is even higher at 50%, as national targets take into account factors such as a member state’s GDP. Although Finland’s current target level is high compared to other EU countries, it is achievable, considering Finland’s self-declared goal of becoming carbon-neutral by 2035.

In 2022, the Emission Trading Directive was updated to also cover maritime transport, road transport, building heating, and industrial fuel use. This has created overlaps with the current effort sharing sector’s coverage.

Objective of the Chemical Industry

The chemical industry supports ambitious climate goals, but policy should also support the implementation of a nature-positive carbon-neutral chemical industry roadmap. In principle, legislative work should be long-term, so changes should be made moderately in future updates, such as when setting the 2040 targets. According to the chemical industry, the boundary between the effort sharing sector and the emissions trading sector should be clarified in the future. When setting the effort sharing sector’s target, a fair distribution among EU member states should be considered, and the procedure should better account for each member state’s potential to reduce emissions. Additionally, any EU-wide support should be equally available to all member states.

The Commission should not be given too much power to compel member states to take action through the governance regulation. This is currently a significant risk, especially concerning conflicting reduction targets in the Energy Efficiency Directive. The Commission should allow member states to implement climate measures as flexibly as possible and not try to force member states into the same mold.

The calculation of carbon dioxide emissions between the emissions trading sector, effort sharing sector, and land-use sector is currently inadequate. It is of paramount importance that sustainable carbon cycle solutions, such as carbon capture, are correctly calculated and considered within the entire legislative framework. All other possible sustainable non-virgin fossil carbon sources should be favored, and legislative barriers related to them should be removed. Such carbon sources include all captured carbon dioxide, all recycled/reused carbon, and sustainable bio-based carbon sources.

In the bigger picture, the Commission should focus on setting 2040 targets and correcting current flaws instead of opening up the 2030 targets.

Current Situation and Timeline

The effort sharing regulation was updated in 2023. The Effort Sharing Regulation is likely to be updated concerning the 2040 targets and rules after the summer 2024 European elections. We influence Finland’s position, Parliament, and the Commission, Cefic’s position, and the Commission’s work program. We monitor the positions of other countries.

Additional information and materials:

Tuomas Tikka

Chief Advisor, Energy and Climate +358 45 131 6683 tuomas.tikka(a)kemianteollisuus.fi Show infoSubject Overview

The Emission Trading Directive is one of the European Union’s main tools to reduce greenhouse gas emissions within the EU. The directive covers the entire energy-intensive industry and all energy production units with a capacity of over 20 MW. In 2022, it was expanded to include maritime transport, and later waste incineration. In the same context, a separate emission trading system for fuel distributors was outlined, which would apply to road transport, building heating, and industrial use. Afry has estimated that including maritime transport in emissions trading would increase transportation costs for export industries (all export sectors combined) by 146 – 291 million euros per year.

Operators within the emissions trading system must account for each ton of emissions generated with emission allowances. The number of emission allowances issued decreases each year, effectively capping emissions. The Emission Trading Directive includes several important points for the chemical industry, such as the definition of sectors vulnerable to carbon leakage, rules for calculating free allowances, and regulations related to emission trading compensation.

Objective of the Chemical Industry

The chemical industry welcomes ambitious climate goals and believes that the emission trading system is a cost-effective way to reduce emissions. However, this requires sufficient carbon leakage protection as long as carbon dioxide emissions are not globally priced equitably.

When raising the emission trading sector’s targets, it is important to ensure the competitiveness of the industry with adequate carbon leakage protection, such as free emission allowances and emission trading compensation. Only a competitive industry can innovate. If there are insufficient free emission allowances for industry, rather than using a multi-sector correction factor, the auction share and the share of free emission allowances should adapt to the industry’s needs, or emission allowances should be made available from the market stability reserve. One-time reductions are not needed either. Emission trading compensation should continue in Finland after 2025, and the Commission’s calculation criteria should be revised to ensure sufficient protection for the industry.

The chemical industry is concerned that the expansion of emissions trading to maritime transport and the new emission trading system related to fuel distributors (ETS2) do not adequately consider the potential impact on industry costs in Finland. The new and separate emission trading system related to fuel distributors (ETS2) should be kept as a separate system for now. Overlaps with the current emissions trading system should be carefully avoided. The expansion to maritime transport seems to burden Finland the most among EU countries, as its exports are largely dependent on maritime transport. Auction revenues from maritime transport would largely end up with inland states that have no interest in developing maritime transport. Additionally, the current directive only partially takes into account northern maritime conditions. The effects of these changes should be closely monitored, and necessary adjustments should be made at the national and EU levels.

The introduction of a carbon border adjustment mechanism will mean a reduction in free emission allowances for sectors covered by the mechanism. Industries entering the mechanism should be provided with a sufficiently long transition period for free emission allowances to allow companies to adapt to the changes. For exports outside the EU, not covered by the mechanism, full emission allowances should be granted.

Addressing the Deficiencies in Enabling Sustainable Carbon Cycles

The flaws related to enabling sustainable carbon cycles should be corrected in the Emission Trading Directive. Emissions should be correctly calculated in all circumstances. The requirement for permanent sequestration leads to double counting for short-lived products. Additionally, negative emissions should be accounted for. Carbon removal certificates could potentially be used for this purpose.

In the bigger picture, the Commission should focus on setting 2040 targets and correcting current flaws instead of opening up the 2030 targets.

Current Situation and Timeline

The current update of the Emission Trading Directive is based on the 2022 update. The national implementation of the directive began in 2023. At the same time, the Commission started preparing several clarifying provisions. The directive’s changes will come into effect gradually, with most of them in place by the end of 2025. The Emission Trading Directive is likely to be updated concerning the 2040 targets and rules after the summer 2024 European elections.

What We Influence

We influence Finland’s position, Finland’s implementation processes, the European Parliament, the Commission, as well as Cefic’s positions, and the future Commission work program. We monitor the positions of other countries.

Additional information and materials:

Emissions Trading Directive (consolidated version).

Tuomas Tikka

Chief Advisor, Energy and Climate +358 45 131 6683 tuomas.tikka(a)kemianteollisuus.fi Show infoSubject Overview

The current EU greenhouse gas reduction target of 55 percent by 2030 is based on the 2020 climate law. In practice this high-level target is divided into sub-targets for the emissions trading sector, burden-sharing sector, and land-use sector. In addition, specific targets have been set for some other climate goals as well e.g. energy efficiency, renewable energy, and biofuels etc.

In February 2024, the Commission published a communication which proposes -90% greenhouse gas target for 2040. The initiative was ambitious, but also in line with industrial targets in Finland. The goal of the chemical industry federation of Finland is to be nature-positive and carbon-neutral by 2045 as part of its voluntary responsibility program, and work towards this goal is already underway.

At the same time, the Commission also published another communication on industrial carbon management (ICM), which describes the role of carbon and specifically the role of carbon capture in the future and also 2040 climate framework.

The Council will discuss the climate target and the desired level of ambition during the spring and summer 2024. The next commission will propose more detailed level climate and energy regulation after the elections.

There have been some differences between member states in the methods how to reduce emissions. A good example of this is nuclear power, which has strongly divided opinions, especially between Germany and France. In addition, there has been significant differences between ambition levels of some member states.

EU’s climate policy and targets are ambitious in global comparison. Therefore, carbon leakage protection has also been a significant topic of discussion, as stricter climate policies may also cause production and investments to move outside the EU.

Objective of the Chemical Industry Federation of Finland

The Chemical Industry Federation of Finland welcomes ambitious energy and climate targets, however there is certain crucial conditionalities. Industry needs adequate carbon leakage protection as well as an environment and political measures which promotes the green transition and investments.

The green transition means electrification, hydrogen economy, and new raw material sources, which require energy and especially clean, stable, and competitively priced electricity. The competitiveness of the industry and investments in the transition towards carbon neutrality must be ensured.

It’s good that the Commission is focusing on setting 2040 targets rather than opening up 2030 targets. Recognizing the importance of carbon cycles is also a step in the right direction.

If the legislation will be revised the CIFF recommends fixing the following issues:

- In the implementation of the Energy Efficiency Directive, it would be important to ensure the adequate availability of clean energy. The energy consumption cap should be removed.

- The Energy Taxation Directive should ensure the competitiveness of industry and especially fair tax treatment for electricity, hydrogen, and climate-friendly fuels.

- The legislative framework should favour the development of a hydrogen economy including green hydrogen as well as other emission-free ways of producing hydrogen and low carbon hydrogen. By-product hydrogen should be acceptable and comparable to renewable hydrogen.

- Nuclear power should be recognized better and accepted as a key climate-friendly energy technology.

- The Emissions Trading Directive (ETS) and carbon border mechanism (CBAM) must ensure adequate investment leakage and carbon leakage protection for export industry. The current carbon border mechanism has practically weakened export protection.

- The state aid rule for emission trading compensation should be reviewed and expanded to cover electricity-intensive chemical industry better.

The chemical industry does not believe that the new emissions trading system for fuel distributors would have the desired impact. The chemical industry supports clear and long-term measurements which are best implemented in the effort-sharing sector through distribution obligations. However, it must be ensured that the competitiveness of the industry and industrial transports are maintained at the same time. One solution would by cutting overlapping taxes and charges.

Additional information

Tuomas Tikka

Chief Advisor, Energy and Climate +358 45 131 6683 tuomas.tikka(a)kemianteollisuus.fi Show infoSubject Overview

The Energy Efficiency Directive sets goals for energy efficiency but also imposes a cap on energy use. Additionally, the directive includes obligations for member states to implement measures to improve energy efficiency and report on efficiency improvements.

Objective of the Chemical Industry

In the future, the industry will need more emissions-free energy as many climate-friendly technologies and solutions are energy-intensive, especially electricity-intensive, such as electrolyzers needed for the hydrogen economy, carbon capture and utilization (CCS/CCU), and power-to-X technologies. Greenhouse gas emissions have already been capped in Europe, so the production and use of emission-free energy needed for new solutions should not be restricted. Therefore, the Energy Efficiency Directive should focus on energy efficiency rather than setting an upper limit on energy use.

The chemical industry is concerned that, based on the climate plans of previous member states, energy use targets have been extremely challenging. The Commission should abandon current unrealistic tightening measures. The Commission should also not jeopardize member states’ green transitions with additional obligations related to energy use if a member state is not reaching its energy use target.

Finland has a long tradition of energy efficiency agreements between the government and the business sector, which have produced good results. During the current agreement period, chemical industry plants have reported energy efficiency improvements totaling 1127 GWh/year by 2021. According to the chemical industry, energy efficiency agreements should continue to serve as a means to meet the requirements of the Energy Efficiency Directive and environmental permit energy efficiency requirements.

Current Situation and Timeline

The Energy Efficiency Directive was updated in 2022, and national implementation began in 2023. The directive is likely to be further updated in 2024 as part of the Commission’s work program after the European elections in the summer of 2024.

Energy efficiency agreements in Finland will be updated for the period after 2025, likely in 2023-2024.

What We Influence

-

Finland’s stance

-

Parliament and Commission

-

Cefic’s position

What We Monitor

- Positions of other countries

Additional information and materials:

Tuomas Tikka

Chief Advisor, Energy and Climate +358 45 131 6683 tuomas.tikka(a)kemianteollisuus.fi Show infoSubject Overview

The Energy Taxation Directive (ETD) establishes common tax principles and minimum tax rates for energy taxes in EU member states. The directive also specifies allowed derogations from tax practices, such as tax exemptions for energy-intensive industries, tax exemptions for bio-based energy, and country-specific exceptions. Changes to the Energy Taxation Directive require unanimous approval in the Council, making attempts to update the directive challenging. Recent attempts have failed, and the content of the 2003 directive no longer adequately reflects the current situation. For example, it does not recognize new climate-friendly fuels.

Objective of the Chemical Industry

The chemical industry believes that the Energy Taxation Directive should ensure competitive tax rates for the industry. The current distinction between tax rates for industry and other uses should be maintained. The current directive does not explicitly mention bio fuels and other low-emission fuels, causing them to be compared to fossil fuels. The chemical industry appreciates the Commission’s proposal to expand the directive to cover new fuels. However, energy taxation should favor all climate-friendly fuels and energy forms equally.

The taxation of climate-friendly hydrogen should be moderate and should apply only at the final consumption stage. Multiple taxation should be avoided, as has been done with electricity taxation. Hydrogen production from raw materials should also be exempt from energy taxation. Additionally, there should be no electricity tax on hydrogen production.

The current directive allows for moderate levels of taxation on industrial electricity. It is crucial to maintain the current EU minimum level of electricity tax for industry. Industrial process use should continue to be exempt from taxation. When updating the tax system, it is essential to identify overlaps, such as the carbon dioxide-based tax component, which would duplicate emissions trading.

Current Situation and Timeline

The Commission published a proposal for the Energy Taxation Directive in 2021, followed by discussions in the Council.

What We Influence

-

Finland’s stance

-

Commission and Council

-

Cefic’s stance

What We Monitor

-

Positions of other countries

-

Positions of other associations

Additional information and materials:

Tuomas Tikka

Chief Advisor, Energy and Climate +358 45 131 6683 tuomas.tikka(a)kemianteollisuus.fi Show infoSubject Overview

The Commission published the so-called Gas Package on December 15, 2021, as part of the overall update of the 2030 targets. The Gas Package includes the following legislative proposals:

- Gas Market Directive

- Gas Market Regulation

- Methane Regulation

Additionally, the package includes a communication on sustainable carbon cycles.

In summary, the Gas Package expands legislation related to natural gas to also cover hydrogen. A significant portion of the legislation relates to gas markets, member state obligations, network rules, and more.

From the perspective of industries using hydrogen, the package also includes important definitions of “low carbon,” certification for low-carbon hydrogen, and aspects related to hydrogen quality. The Gas Package complements the definitions of hydrogen in the Renewable Energy Directive.

The crucial aspect of the package is the potential additional costs brought about by the legislation and how they are distributed.

Objective of the Chemical Industry

The chemical industry aims to ensure that Finnish and EU legislation does not hinder the progress of the hydrogen economy and that there is sufficient research, development, and investment funding to kickstart the hydrogen economy and make the technologies commercially competitive. Additionally, any potential disruptions and additional costs for existing market participants must be avoided.

Having a clear definition of low-emission hydrogen is crucial to kickstarting investments. Furthermore, hydrogen produced using nuclear power should be acceptable.

The Gas Directive does not seem to provide entirely clear answers to hydrogen definitions. It defers more detailed definitions to delegated regulations. The chemical industry believes it would be better if the directive (or regulation) could specify the definition of low-carbon hydrogen and certification-related issues rather than delegating them to subordinate regulations.

The Gas Regulation includes a requirement for member states to accept hydrogen blended with natural gas. From the chemical industry’s perspective, a lower proportion (less than 5% proposed by the Commission) would be more sensible to avoid potential concentration fluctuations that could disrupt the processes of companies using natural gas. It is currently unclear whether mixing hydrogen will affect market operations and whether adding hydrogen will result in additional costs for gas users.

The chemical industry believes that the quality of gas must be guaranteed for companies, and additional costs must be avoided if possible. If legislation does lead to additional costs, they should be distributed fairly.

Current Situation and Timeline

The Commission published the Gas Package at the end of 2021, followed by further discussions in the Council and Parliament in 2022 and 2023. Trilogue negotiations began in the summer of 2023.

What We Influence

-

Finland’s stance

-

European Parliament and Commission

-

Cefic’s stance

-

The activities and positions of the hydrogen cluster

We monitor the positions of other countries and stakeholders and influence the implementation of the legislation.

Additional information and materials:

Commission’s proposal for the Gas Package.

Tuomas Tikka

Chief Advisor, Energy and Climate +358 45 131 6683 tuomas.tikka(a)kemianteollisuus.fi Show infoText here

Tuomas Tikka

Chief Advisor, Energy and Climate +358 45 131 6683 tuomas.tikka(a)kemianteollisuus.fi Show infoSubject Overview

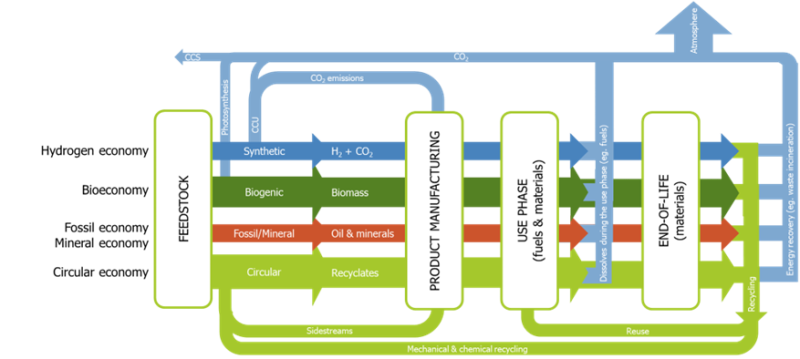

In the future, the chemical industry will require a huge amount of alternative raw material sources, to replace virgin fossil raw materials and energy. Alternative sources include all captured carbon dioxide, recycled/reused carbon (waste), and sustainable bio-based carbon sources. In addition, the chemical industry will need significant amounts of renewable and low-carbon hydrogen. On the inorganic chemistry side, there is a great need to find the best material solutions. A good example is the growing need of batteries and battery chemicals where the recycled materials are the only viable option to subsidy virgin raw materials. Decreasing the share of virgin fossil raw materials will often reduce the dependence on the imported raw materials and therefore increase material and energy security.

Modern production plants are very efficient and different kind of waste heat, waste, and residues are utilized effectively. Chemical industry raw materials can also be produced synergistically with other segments. For example, more extensive use of biomass as a raw material in the chemical industry can increase its overall value and benefit food/feed production and renewable energy production. The chemical industry produces a wide range of products and fuels for other sectors, so finding alternative raw materials is also critical for the carbon neutrality of other industries.

The development processes for new raw materials have been going on for some time and new sources have been found and adopted whenever possible. The work has been challenging because each new source must be carefully evaluated. Often restricting factors and/or other challenges are found during the evaluation. For example, potential raw material might be very climate friendly, but challenging from biodiversity perspective.

The incompleteness of legislation and current flaws also slow down the transition and at worst remove the basis for investments altogether. In addition, the cost difference between virgin fossil raw material and alternative raw material is often a significant obstacle. On the product side, this is reflected as a lack of demand.

Current legislation does not recognize and support the alternative raw materials which slows down the transition and, at worst, completely prevent investments. The cost difference between virgin fossil raw material and alternative raw material is often a significant obstacle, which reflects as a lack of demand of alternative raw material products.

The Commission published a communication on industrial carbon management (ICM) and 2040 climate targets in February 2024. The ICM communication describes the role of carbon capture, storage and utilization in the future, as a part of the 2040 climate framework. The role of carbon cycles seems to be connected better in the climate policy framework and this is expected to be reflected in further discussions.

Objective of the Chemical Industry Federation of Finland

Key messages

- The EU must develop a sufficiently comprehensive Circular Carbon Strategy that covers all alternative carbon cycles (recycling, bio, (B)CCU)

- Existing legislation must be amended to recognize and support alternative carbon sources:

- Legislative sectors must be harmonised to recognise all alternative carbon sources and support all carbon cycles

- Climate legislation must be fixed. The most crucial parts seem to be:

- ETS including CCU rules and emission accounting rules, which must clear and favour fairly (B)CCU products.

- Renewable energy directive (RED) covering crucial hydrogen rules and sustainability criteria’s which should be harmonized to cover all products.

- Carbon removal certificates should promote alternative carbon cycles fairly

- New market incentives should be developed for alternative carbon products.

- Funding and subsidies are crucial to accelerate massive investments

- Focus on EU-level mechanisms instead of subsidy race between EU member states For example, carbon bank seems to be promising mechanism.

- Only competitive industry can invest and move towards carbon neutrality.

More detailed messages

All alternative sustainable carbon sources should be favoured over virgin fossil raw materials, and legislation should support this principle. There is a clear need to for alternative carbon product markets in EU. The EU therefore needs to ensure that sufficient comprehensive Circular Carbon Strategy will be prepared. This strategy should support all technologies that are need for circular economy and different carbon loops (chemical and mechanical recycling, (B)CCU technologies, bio-based carbon sources etc). It is also important to remember technology neutrality when promoting alternative carbon sources.

CO2 calculation rules in the emissions trading sector, effort sharing sector and land-use sector are currently inadequate. For example captured carbon or negative emissions are not properly accounted in ETS. In addition, current life cycle modelling calculations are not treating raw material sources fairly.

The Commission has identified ETS as one of the key legislations in the future. It is crucial to fix the calculation rules so that technologies related to CCS/U would become more common and new raw material alternatives could become reality. In addition, the role of carbon removal certificates should be clarified. These certificates could be used to connect carbon removals to the ETS, which might solve some challenges related to calculation rules.

In addition to correcting the existing legislation, the Commission should develop markets for products based on alternative carbon sources. Especially EU should consider different kind of incentives for alternative carbon products.

Too strict technology guidance is not needed. However, in certain situations, it is justified to promote certain new technologies or environmentally friendly products. For example, the double counting for the advanced biofuels category is justified in order to bring advanced fuels into wider use.

The legislative framework should favour the development of a hydrogen economy including green hydrogen, low carbon hydrogen and other climate friendly possibilities. By-product hydrogen should be acceptable and comparable to renewable hydrogen. Sufficient flexibility must be maintained in the use of weather-dependent renewable energy for RFNBO (green hydrogen).

It is important that the sustainability criteria’s for renewable fuels are kept unchanged to maintain the operational capability of current and planned investments. Long-term and predictable politics are essential for industrial investments. Sustainability criteria could be harmonized to cover other bio-based products too. This would require simultaneous arrangements to ensure incentives for new alternative carbon products.

Funds and subsidies will be in crucial role when pushing massive investments forward. EU-level innovation-, investment- and maybe even product subsidies are important as long as the new production methods are more expensive when compared to existing virgin fossil products. It is also essential to maintain access for all EU member countries to funding mechanisms and avoid unfair national funding competition among member states. For example, a “carbon bank” type of EU-fund could be justified from this perspective. New market incentives are also needed to support demand for products made from sustainable alternative raw materials.

For small member states like Finland, it is important to abandon flexible state aid rule exceptions which implemented during the pandemic years. Funding should be based on fair EU-wide state aid rules and criteria’s.

Only a competitive industry can face/survive the raw material revolution challenge and successfully adapt it’s processes to future raw material demands. More precise information can be found from the CIFF 2040 onepager.

Tuomas Tikka

Chief Advisor, Energy and Climate +358 45 131 6683 tuomas.tikka(a)kemianteollisuus.fi Show infoSubject Overview

The Renewable Energy Directive sets EU-wide targets for renewable energy that the EU and its member states must achieve by 2030. Additionally, the directive defines criteria for sustainable renewable energy sources and fuels and regulates guarantees of origin. The definitions of renewable energy are crucial for chemical industry companies in terms of the acceptability of current and especially new fuel types and energy sources. The likely next update will involve setting targets for 2040.

Objective of the Chemical Industry

According to the chemical industry, setting targets for renewable energy should promote rather than hinder the carbon-neutral development of the industry.

The Renewable Energy Directive should identify new energy sources and production methods as widely renewable, such as new synthetic fuels and hydrogen technologies. It is crucial to favor all renewable and low-carbon investments as widely as possible and not inadvertently hinder investments by favoring various technologies too restrictively.

The need for investment support will be enormous. New mechanisms, such as the Carbon Contracts for Difference (CCfD), should be considered alongside existing support mechanisms. However, it is essential to maintain access to support for all member states within the EU and avoid inter-member state competition for support.

Excess heat and useful by-products such as hydrogen are often generated in industrial processes. Utilizing these sources should be acceptable and equivalent to renewables.

Excessively stringent technological guidance is unnecessary. In some cases, it is justified to target legislative guidance to promote certain new technologies or climate-friendly products. For example, double-counting in the advanced biofuels category is justified to expand the use of advanced fuels. Otherwise, coefficients should be abandoned, and the focus should be on actual emissions reductions rather than calculations.

In the bigger picture, the Commission should focus on setting 2040 targets and correcting current flaws instead of opening up the 2030 rules.

Current Situation and Timeline

The Renewable Energy Directive came into force in 2023, and member states began implementation in the same year. The directive is likely to be updated concerning the 2040 targets and rules after the summer 2024 European elections as part of the Commission’s work program.

We influence Finland’s position, the European Parliament, and the Commission, as well as Cefic’s position. We monitor the positions of other countries.

Additional information and materials:

Tuomas Tikka

Chief Advisor, Energy and Climate +358 45 131 6683 tuomas.tikka(a)kemianteollisuus.fi Show infoSubject Overview

SCC, or Sustainable Carbon Cycles, is the Commission’s approach to consolidating various policy areas related to sustainable carbon cycles under one heading. The term itself originates from the Commission’s vision, which materialized in a communication paper bearing this name in 2021.

In practice, the Commission’s vision focuses significantly on land use and carbon farming but also includes the goal for industries to use 20% non-fossil raw materials, as well as the EU-level target to capture 5 million tons per year of carbon dioxide from the atmosphere. Following the communication, the Commission presented a proposal for carbon removal certificates, which seems to be primarily aimed at capturing biogenic carbon dioxide and directly capturing carbon dioxide from the atmosphere.

Sustainable carbon cycles are a cross-cutting theme spanning several policy areas, and related legislation can be roughly categorized into three categories: climate legislation, legislation related to biogenic carbon, and legislation related to waste-based raw materials.

Key legislation includes:

- Climate: Emission Trading Directive, CCS Directive, burden-sharing regulation, net zero industry act, carbon removal certificates (including bio), Energy Taxation Directive, taxonomy,

- Bio: Renewable Energy Directive, LULUCF,

- Waste: Waste Framework Directive, Packaging Waste Regulation, Ecodesign for Sustainable Products Regulation (ESPR), End of Life Vehicles Regulation, Construction Products Regulation

Objective of the Chemical Industry

The chemical industry aims for greater clarity and harmonization in the current extensive legislative framework. Moreover, the authorities responsible for different legislative blocks should have a sufficient understanding of the overall picture.

One significant issue with current legislation is that it does not sufficiently promote alternative sustainable sources of carbon to virgin fossil raw materials. This is particularly evident in climate-related legislation, which does not favor carbon dioxide capture and reuse. Typically, legislation requires carbon to be permanently sequestered in the product. If this does not occur, the legislation usually penalizes carbon capture and utilization (CCU) as double counting of emissions. Additionally, some legislation does not recognize negative emissions. Similar challenges exist in the field of material recycling. Legislation should favor keeping carbon in circulation through mechanical and chemical recycling methods instead of landfilling or incinerating waste, but this is not currently happening.

Accurate accounting and consideration of emissions are essential for achieving sustainable carbon cycles. Accounting presents significant challenges in many cases, partly due to the different policy areas. For example, carbon dioxide emissions are divided into the emission trading sector, the burden-sharing sector, and the land use sector. Sustainable carbon cycles cannot be confined to a single sector, as they may extend to several sectors depending on the situation.

The chemical industry believes that the Commission’s proposed objectives should be properly promoted. However, these objectives should remain sufficiently high-level in the future. At its simplest, the objective could be a percentage of the use of alternative sustainable carbon sources over virgin fossil ones. Such carbon sources could include all captured carbon dioxide, recycled/reused carbon, and sustainable biogenic carbon sources.

Regardless, substantial investments will be needed, so support programs and state/state-owned company investments (e.g., in infrastructure) will be necessary. However, the promotion of sustainable carbon cycles should be technology-neutral.

Key Messages from the Chemical Industry:

-

The extensive legislative framework should be harmonized and consistent.

-

Fair and just accounting rules are needed; the product’s lifecycle length should not affect the calculation; negative emissions should be considered.

-

Legislation should favor all sustainable alternative carbon sources over virgin fossil sources, which should also be reflected in the objectives.

-

Investments should be supported rather than penalized; technology neutrality is crucial.

Current Situation and Timeline

The Commission published a communication on sustainable carbon cycles at the end of 2021. Subsequently, the Commission has released a regulation related to carbon removal certificates, which has been under consideration by the Parliament and the Council in 2023. Sustainable carbon cycles are likely to be part of the Commission’s work program to be selected in 2024.

What We Influence

- Finnish authorities and politicians

- The EU Commission and Parliament

- Cefic, NorBal, and other stakeholders with similar interests

- The Commission’s work program following the 2024 elections

We also monitor the positions of other countries.

For more information and materials:

Tuomas Tikka

Chief Advisor, Energy and Climate +358 45 131 6683 tuomas.tikka(a)kemianteollisuus.fi Show infoLabour law, know-how and education

Subject overview

Starting from the premise that the funding for vocational education in the field of technology should cover its implementation costs, financing should take into account investment-intensive learning environments, machinery, and equipment. Funding should also be available for joint learning environments between the workforce and educational providers, in line with the spirit of the revamped vocational education law.

In the vocational education reform, a focus was placed on work-life orientation and workplace learning, individualized paths, and competence-based approaches, resulting in accelerated studies. However, funding remained fragmented and challenging to predict.

The challenges in vocational education within the field of chemistry include low attractiveness and poor employment prospects for graduates of basic vocational programs, all while the competency needs in the chemical industry are growing and diversifying.

Objective of the Chemical Industry

The relevance of funding for technology-related fields will be reviewed. The weight of feedback from the workforce will be increased in funding decisions, as promised during the law’s reform.

In the future, funding criteria should be adjusted to consider not only short-term realized costs but also other training cost metrics. Funding planning should take into account the specific characteristics of expensive training fields.

The entire vocational education funding system needs to be made more understandable, predictive, and supportive of vocational education’s role in the workforce.

Implementing vocational education reform; involving businesses and making learning flexible. Creating new learning environments in collaboration with companies.

English-language accreditation for vocational education should be granted whenever there is a need for skilled workers in a particular field, and local companies are involved in the applications.

Anni Siltanen

Chief Advisor, Skills and Competence +358 44 562 5991 anni.siltanen(a)kemianteollisuus.fi Show infoFinnish industry actively works to secure Finnish future expertise. In the future, we need the best possible experts for businesses to secure renewal and growth towards a carbon-neutral future. Expertise in natural sciences and mathematics (LUMA) is one of the most important skills needed by the industry. The National LUMA Strategy responds to the long-term development of expertise needs.

Goals of the chemical industry:

- We closely monitor the implementation of the LUMA Strategy. The implementation of the LUMA Strategy must respond to the industry’s expertise needs, especially when considering the increased need for LUMA expertise due to the transition to carbon neutrality. Finnish LUMA expertise will increasingly compete in global markets in the future. Finland must remain a leading country in LUMA expertise, and PISA results must be improved.

- An objective impact assessment will be carried out for LUMA-CENTER Finland. The LUMA Finland network has been doing valuable work in promoting natural sciences and mathematical capabilities for almost a decade, but its impact has not been objectively studied.

Anni Siltanen

Chief Advisor, Skills and Competence +358 44 562 5991 anni.siltanen(a)kemianteollisuus.fi Show infoEnvironment, health and safety

Subject Overview

Biodiversity is a globally emerging topic alongside climate issues. For example, the World Economic Forum has estimated that over half of the world’s GDP depends on nature. In the fall of 2022, at the UN Montreal-Kunming Biodiversity Conference, it was decided to protect 30% of the Earth’s surface by 2030, along with other measures to strengthen declining biodiversity. In connection with the EU Green Deal, the EU’s biodiversity strategy was published, with the goal of restoring European biological diversity by 2030 for the benefit of people, the climate, and the planet. Biodiversity is now playing a new role in EU decision-making and may affect, for example, permits for chemical industry companies or raw materials. Nationally, biodiversity has also become a pressing issue and is reflected in legislation, such as the recently revised nature conservation law, which includes voluntary ecological compensation.

The Goal of the Chemical Industry

The goal of nature-positive, carbon-neutral chemistry by 2045 was set as the first milestone in biodiversity work in August 2022. During the spring of 2022, the role of the chemical industry in relation to biodiversity was examined, leading to an action plan and a timeline similar to a climate roadmap. Through impact assessments, we also gain a better understanding of how the chemical industry should engage in advocacy issues related to biodiversity. Another important goal is to increase awareness among companies regarding biodiversity, such as through training and guides provided to businesses. The aim is for 70% of chemical industry member companies to set biodiversity goals in their strategies by 2025. In addition, the chemical industry actively participates in the development of global terminology.

We influence by:

- Contributing to the development of the ISO SFS Biodiversity standard.

- Raising awareness on the topic in Cefic.

- Highlighting the nature-positive perspective in our national advocacy and statements.

- Internally, through a Biodiversity ad hoc group composed of representatives from member companies.

- Sharing best practices through the Responsible Care program.

We monitor:

- The EU Business and Biodiversity platform.

- The ICC Biodiversity working group.

- EU-level discussions in the Commission and Parliament.

Current Situation and Timeline

The goal has been set. Next, we will raise awareness among companies, participate in the development of the ISO Standard, share best practices, and advance nature-positive, carbon-neutral chemistry!

Additional information:

The 2022 Montreal-Kunming agreement

EU Biodiversity strategy 2030

Johanna Pentjärvi

Senior Advisor, Responsibility +358 40 570 3920 johanna.pentjarvi(a)kemianteollisuus.fi Show infoThe national implementation of the CER directive approved by the EU is underway. The directive pertains to the resilience of nationally important companies in the face of disruptions. A Finnish legislative proposal is expected to be ready for review by the end of 2023. The law is set to come into effect on October 18, 2024, pending approval by the parliament in the spring of 2024. Together with the NIS2 directive, the CER directive forms the basis for preparedness against security threats.

It is not yet known which companies will fall under the scope of the law. The law will categorize companies it applies to as either essential or important. Essential companies will be required to report in advance to the authorities. Important companies will be inspected by the authorities based on their own schedules. In general, the categorization of companies will follow the NIS2 directive.

The law’s requirement for companies to prepare for various security threats is broad and challenging to implement because it is unknown what kinds of threats criminal entities may pose to companies in the future. The successful implementation of the law requires strong cooperation between companies and authorities. Authorities must first conduct a national risk assessment. Based on national risk assessment companies falling under the scope of the law will conduct company-specific risk assessments. Due to these risk assessments and the resulting actions, it is likely that the law will have long transition periods.

Kemianteollisuus ry (Chemical Industry Federation of Finland) is monitoring the progress of the law’s preparation through stakeholder events, organizing information seminars for member companies, and communicating the perspectives of the chemical industry to the lawmakers.

The revised Dangerous Substance Transport Act (Vaarallisten aineiden kuljetus, VAK Act, in Finnish) came into effect on September 1, 2023, and it now forms a comprehensive framework for requirements in all four modes of transportation – road, rail, maritime, and air transport. The goal is to streamline regulations, eliminate ambiguity, and address deficiencies. Finland’s national VAK Act is now more aligned with international regulations. Above all, the law aims to enhance transportation safety in Finland.

The VAK Act is extensive and covers a wide range of activities. In addition to the VAK Act and its related regulations, more detailed guidance will be needed from the Finnish Transport and Communications Agency on how operators should proceed in specific situations. Furthermore, the regulatory oversight responsibility will shift to the authority (Traficom). These changes emphasize the growing involvement of the authority in transportation safety and increased collaboration between businesses and authorities.

The law establishes uniform standards for the temporary storage of dangerous substances. Emergency plans and safety assessments prepared for this purpose enhance the ability of both businesses and authorities to respond to hazardous situations and, most importantly, help prevent them. However, this also requires more effort and resources from all parties involved.

The law places significant emphasis on the chemical and safety expertise of both drivers and companies responsible for transportation. The role of safety advisors in companies becomes more crucial.

Subject Overview

The purpose of renewing legislation on batteries and accumulators is to modernize the legal framework to better align with a new operational environment. The regulation was published on January 20, 2023, and it replaces the previous battery directive. This regulation is part of the European Green Deal and includes various targets to be implemented in different years, such as those related to the collection, recycling, and labeling requirements for batteries.

The Goal of the Chemical Industry

The development and production of batteries are crucial growth factors in Europe, and significant investments are planned for the near future. The goal is to develop the entire battery value chain within the EU, covering sustainable mining and refining of materials, battery cell manufacturing, and recycling business. The objective is to promote the business activities of Finnish companies in the battery industry throughout the entire value chain.

Pia Vilenius

Chief Advisor, Bioeconomy and Circular Economy +358 40 413 6340 pia.vilenius(a)kemianteollisuus.fi Show infoSubject Overview

In the fall of 2020, the Commission released a sustainability-focused chemicals strategy (Chemicals Strategy for Sustainability). The goal of the chemical strategy is to enhance chemical safety and support the production, innovation, and investments in chemicals aligned with sustainable development. The core of the strategy consists of around 60 different legislative proposals related to REACH registrations, expanding the control of substances of concern, restrictions based on substance properties, and new chemical classifications. Some of the proposals have already been implemented as regulations, and the target timeline for the full implementation of the strategy is by the year 2024.

Objective of the Chemical Industry

The industry’s concerns revolve around the predictability of regulations and adherence to the principles of better regulation. Pushing through dozens of legislative proposals within a tight schedule, as outlined in the strategy, requires substantial resources both from the Commission and national authorities. Especially, the assessment of the proposals’ impacts may remain superficial, as well as ensuring the cost-effectiveness and scientific basis of the proposed actions and demonstrating their safety-enhancing effects.

It is also important to initiate actions that support innovation, maintain strategic value chains and production within the EU, provide funding for the promotion of safe and sustainable products, and invest in skills development. In the implementation of the numerous legislative proposals of the strategy, the focus should be on those that can genuinely enhance safety. Resources within companies, authorities, and EU institutions are limited. Therefore, the preparation and implementation of proposals should be prioritized and phased to adhere to the principles of better regulation. The strategy includes various framework terms, such as essential uses, safe and sustainable by design, and a general risk-based approach, which need to be defined before they are applied in regulations.

The actions of the chemical strategy should support the goals of the EU’s Green Deal and attract investments for the green transition within the Union. The EU will continue to need safe chemicals, for example, for solutions related to the hydrogen economy, battery technologies, and the circular economy.

Eliisa Irpola

Chief Advisor, Product Safety +358 40 539 2556 eliisa.irpola(a)kemianteollisuus.fi Show infoSubject Overview

The EU’s Industrial Emissions Directive (IED) is one of the fundamental documents for environmental permitting, and its revision has an immediate impact on companies’ environmental licensing obligations. The revision of the directive has been prepared at the EU Commission for a couple of years and is based on the EU Green Deal’s objectives of Zero Pollution, Climate Neutrality, Biodiversity, and a cleaner, more Circular Economy. The Commission published the draft revision of the directive in the spring of 2022. The Industrial Emissions Directive serves as a background directive for Best Available Techniques (BAT) reference documents, which provide regulations on the best available technology for different industries and activities across Europe.

The Goal of the Chemical Industry

The Industrial Emissions Directive is one of the most significant directives guiding the operation of chemical industry facilities. The directive applies to over 80 chemical industry facilities in Finland.

In early summer 2022, a survey was conducted among member companies of the Chemical Industry Association regarding the Commission’s proposal for changes to the EU Industrial Emissions Directive. Generally, companies saw the proposal as quite challenging, partly increasing costs or being impractical without significant or yet nonexistent innovations. On the other hand, there was a perception that the proposal increased bureaucracy, prolonged permit processing times and costs, but still allowed operations to continue, and the costs incurred were somewhat reasonable in relation to the requirements. Companies are most critical of the requirement to apply the strictest possible emission limit values in the permitting process, to the extent that it is feared to negatively impact profitability. Additionally, in line with the nature of the chemical industry, it is simply not possible to push all parameters to the lower limits. For example, if the purification of a certain emission is increased, energy consumption may rise. The Commission’s growing demands for the disclosure of various information have also raised significant concerns within the chemical industry, especially regarding the confidentiality of information, particularly related to business secrets.

Only the promotion of innovations was clearly seen as a positive new opportunity, although there are still uncertainties associated with its key elements, which is why no company was certain about utilizing this opportunity. To enable companies to truly seize the opportunity and promote the emergence of new innovations, the proposal should be further refined. The development of new technology always entails the risk of failure, and this should be addressed in the proposal in a more encouraging rather than discouraging manner.

The Industrial Emissions Directive will expand its scope in many areas. From the perspective of the chemical industry, key decisions concern the battery value chain and hydrogen plants.

The chemical industry has been an active member of the national background group and continues to follow the trilogue negotiations.

Current Situation and Timeline

The European Commission’s proposal for the revised Industrial Emissions Directive was released in April 2022. During the summer of 2023, both the Council and the Parliament reached their general positions. In the fall of 2023, the trilogue phase is expected, which is anticipated to lead to the approval of the directive by early 2024 at the latest. National implementation will begin in early 2024, and member states will have two years to incorporate the directive proposal into their national legislation. In Finland, this largely concerns the Environmental Protection Act.

In connection with the Industrial Emissions Directive, the latest BAT conclusion for waste gases in the chemical industry was published in the fall of 2022. This BAT is currently the most significant BAT for a large portion of chemical industry facilities.

We influence by:

- Participating in the work of the Ministry of the Environment’s national background group.

- Promoting our messages in Cefic working groups.

Additional Information and Materials

Overview of the Industrial Emissions Directive on the European Commission’s website.

Council’s agreement on amendments to industrial emissions directive.

Download the draft proposal here.

Johanna Pentjärvi

Senior Advisor, Responsibility +358 40 570 3920 johanna.pentjarvi(a)kemianteollisuus.fi Show infoThe national implementation of the EU-approved NIS2 directive, which concerns cybersecurity, is underway. Finland’s national legislative proposal will be prepared for review during the year 2023. The law is expected to come into effect on October 18, 2024, so parliamentary approval should occur in the spring of 2024.

This law is an improved version of the old NIS directive. For the chemical industry, the new law is significant because it now falls under the directive’s scope. The law will categorize applicable companies to as either essential or important. Essential companies will be required to report in advance to the authorities. Important companies will be inspected by the authorities based on their own schedules.

The requirement for companies is to prepare for all cyber security threats. In practice, this is challenging and depends greatly on the types of threats that criminal entities may pose to companies in the future. The successful implementation of the law requires strong cooperation between companies and authorities. Additionally, inter-company information sharing is crucial to quickly identify threats.

Kemianteollisuus ry (Chemical Industry Federation of Finland) will monitor the progress of preparation of the law through stakeholder events, organize information seminars for member companies, and communicate the perspectives of the chemical industry to the lawmakers.

Subject Overview

The EU Commission has developed an action plan for Zero Pollution. The goal is to better prevent, manage, monitor, and report on the pollution of water, air, and soil. The aim is also to separate economic growth from an increase in emissions, strengthen the connection between environmental protection, sustainable development, and human well-being, and mainstream the Zero Pollution concept into all regulations.

The Zero Pollution plan serves as a starting point and a cross-cutting idea for future legislative projects. It impacts various initiatives in energy, industry, transportation, agriculture, biodiversity, and particularly climate issues and chemical strategy. Zero Pollution is a key part of the EU’s Green Deal.

The Zero Pollution package includes several draft directives or proposals for revisions, such as the revision of the urban wastewater directive, the drinking water directive, the healthy soil directive, and environmental targets related to water.

The Chemical Industry’s Position

The chemical industry is strongly committed to the principle of “preventing harm to humans and the environment” and continuously seeks to improve by reducing its emissions. This commitment can be verified through our Responsible Care indicators. The products and solutions produced by the chemical industry play a crucial role in achieving the Zero Pollution goal, which, according to the EU Commission, does not mean zero emissions but rather a balance between potential harm and benefits, with a net positive impact.

Crucial for the realization of the Zero Pollution goal is broad cooperation and open dialogue among various stakeholders to create an effective policy framework that enables the significant investments required to implement the Green Deal as a whole. This policy framework should build upon existing and proven legislation.

The chemical industry is closely monitoring the draft proposals for the urban wastewater directive and the directive concerning soil health.

Current Situation and Timeline

The EU Commission released its Zero Pollution Action Plan concept in May 2020. In October 2022, a new Zero Pollution package was published, addressing air quality, urban wastewater, and changes to the substance listings of the Water Framework Directive. In the summer of 2023, a proposal for a directive concerning soil health was published.

Additional information and materials:

Read more on the Zero Pollution Action Plan

SOIL

What This Is About

As part of the EU Green Deal, the EU released the Soil Strategy in 2021, with the vision that by 2050, all EU soil ecosystems will be healthy, requiring determined changes in this decade. As a measure to improve soil quality, the Commission released the Soil Health Directive in the summer of 2023. It includes elements such as regional monitoring of soil conditions, harmonization of soil sampling and analysis, continuous monitoring, principles for sustainable land use, identification of contaminated areas based on risk assessment, and the implementation of risk reduction measures.

The Chemical Industry’s Goal

The chemical industry emphasizes risk-based assessments and actions in various evaluations and activities related to soil. Through anticipation and strong environmental expertise, soil contamination is sought to be prevented using the best possible methods.

Current Situation and Timeline

The European Commission released the Soil Strategy as part of the Green Deal program in 2021. The Commission’s proposal is under consultation in the fall of 2023. The proposal will be discussed in the Parliament and the Council in the fall of 2023, but a more specific timeline is not yet available.

Additional Information and Materials

Commission’s proposal and consultation service.

Johanna Pentjärvi

Senior Advisor, Responsibility +358 40 570 3920 johanna.pentjarvi(a)kemianteollisuus.fi Show info

Sami Nikander

Director, Responsibility +358 40 567 4413 sami.nikander(a)kemianteollisuus.fi Show infoSubject Overview

In the future, the chemical industry will require a huge amount of alternative raw material sources, to replace virgin fossil raw materials and energy. Alternative sources include all captured carbon dioxide, recycled/reused carbon (waste), and sustainable bio-based carbon sources. In addition, the chemical industry will need significant amounts of renewable and low-carbon hydrogen. On the inorganic chemistry side, there is a great need to find the best material solutions. A good example is the growing need of batteries and battery chemicals.

Reducing virgin fossil raw materials will often reduce also the dependence on imports and increase the level of raw material security.

The development processes for new raw materials have been going on for some time and new sources have been found and adopted whenever possible. The work, however, has been challenging as each new source must be carefully evaluated. Often restricting factors and/or other challenges are found during the evaluation.

In addition, the legislation does not support the alternative raw materials which slows down the transition and, at worst, completely prevent investments.

The Commission published a communication on industrial carbon management (ICM) and 2040 climate targets in February 2024. The ICM communication describes the role of carbon capture, storage and utilization in the future, as a part of the 2040 climate framework. The role of carbon cycles seems to be connected better in the climate policy framework and this is expected to be reflected in further discussions.

Objective of the Chemical Industry Federation of Finland

All alternative sustainable carbon sources should be favoured instead of virgin fossil raw materials, and legislation should support this principle. The EU therefore needs to ensure that sufficient comprehensive Circular Carbon Strategy will be prepared. This strategy should support all technologies that are need for circular economy and different carbon loops (chemical and mechanical recycling, (B)CCU technologies, bio-based carbon sources etc).

CO2 calculation rules in the emissions trading sector, effort sharing sector and land-use sector are currently inadequate. For example captured carbon or negative emissions are not properly accounted in ETS. The Commission has identified ETS as a key element in the future climate, but the calculation rules should be fixed so that technologies related to CCS/U would become more common and new raw material alternatives could become reality. In addition, the role of carbon removal certificates should be clarified. These certificates could be used to connect carbon removals to the ETS, which might solve some challenges related to calculation rules.

The legislative framework should favour the development of a hydrogen economy including green hydrogen as well as other emission-free ways of producing hydrogen and low carbon hydrogen. By-product hydrogen should be acceptable and comparable to renewable hydrogen.

Too strict technology guidance is not needed. In certain situations, however, it is justified to target legislation to promote certain new technologies or environmentally friendly products. For example, the double counting for the advanced biofuels category is justified in order to bring advanced fuels

into wider use. Otherwise, multipliers should be abandoned, and real emission reductions should be favoured.

It is important for the chemical industry that the sustainability rules for renewable fuels are kept unchanged to maintain the operational capability of current and planned investments. Long-term and predictable politics are essential for industrial investments.

The need for investment subsidies will be huge. However, it is important to maintain access to subsidies for all member states within the EU and avoid subsidy competitions between member states. For example, a “carbon bank” as a form of support could be justified from this perspective.

Competitive industry enables the raw material revolution and the implementation of carbon cycles. More precise information can be found from the CIFF 2040 onepager.

Chemical Industry Federation of Finland’s statements

Our statements on current topics: